|

Pedestrians in Tokyo pass an electronic board displaying the yield on 10-year Japanese government bonds on Jan. 19. The benchmark yield reached its highest level in 27 years since 1999. AFP/Yonhap. |

SEOUL, Jan 21 (AJP) - Major sovereign bond yields, including South Korean treasuries, jumped on Tuesday after a sharp surge in Japanese government bond yields — bringing the elephant in the room back into focus: the massive yen carry trade.

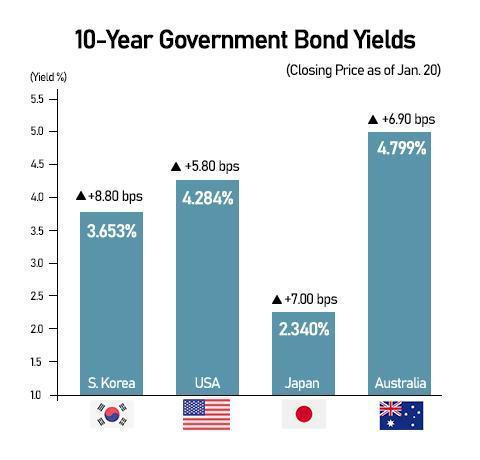

The benchmark 10-year JGB yield closed up 7 basis points at 2.34 percent, its highest level in nearly three decades. The move quickly spilled over abroad, pushing the U.S. 10-year Treasury yield up 7.5 basis points to 4.295 percent and Australia’s 10-year yield up 6.9 basis points to 4.799 percent.

South Korea proved particularly sensitive. The 10-year Korean government bond yield surged 8.8 basis points to 3.653 percent, marking its highest level in almost two years.

|

Graphics by AJP Song Ji-yoon. |

Japan has long functioned as a global liquidity provider, with near-zero borrowing costs encouraging yen-funded carry trades for decades. The recent rise in JGB yields is now prompting capital repatriation, as Japanese investors pull funds back home to capture higher domestic returns.

Because the yen serves as a major funding and reserve currency, this reversal has acted as a destabilizing force for global bond markets.

Notably, the latest spike in yields was driven less by monetary policy than by fiscal concerns.

The Bank of Japan is set to announce its interest rate decision on Friday, and the advanced trigger came from political developments surrounding Prime Minister Sanae Takaichi’s policy agenda.

On Tuesday, Takaichi announced plans to dissolve parliament on Jan. 23 and call snap elections for Feb. 8. Although the ruling coalition of the Liberal Democratic Party and Nippon Ishin no Kai already controls 233 seats, she is seeking at least 240 seats to consolidate legislative dominance.

Markets reacted sharply to her populist stimulus pledges, particularly proposals to cut consumption taxes on food and beverages to 8 percent — a move estimated to create a 5 trillion yen ($31.6 billion) revenue shortfall — without clear funding measures.

Bond yields retreated after Takaichi later pledged that “there will be no additional debt issuance,” with the 10-year JGB yield falling about 8 basis points by Wednesday morning. However, skepticism remains, as yields continue to hover above 2.3 percent and investors question whether stimulus can be financed without new borrowing.

Demand for Japanese debt has already weakened. A recent 20-year JGB auction recorded a record-low bid-to-cover ratio, underscoring investor caution.

|

Generated with Notebook LM. |

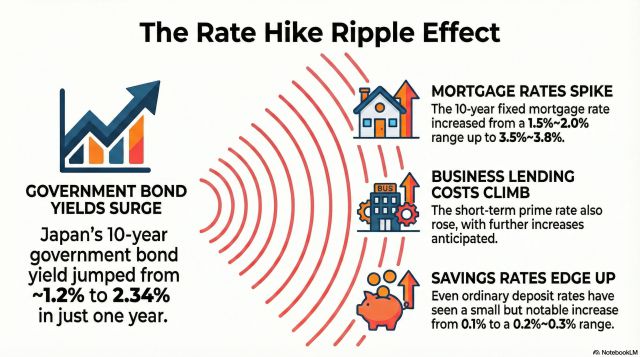

The rise in government yields has filtered through to consumer lending. As of Wednesday, 10-year fixed mortgage rates at Japan’s megabanks — Mizuho, MUFG and SMBC — were approaching 3.8 percent, nearly double the roughly 2 percent ceiling seen a year earlier.

Analysts have compared the episode to the U.K.’s 2022 “Truss Shock,” when unfunded tax cuts proposed by then–Prime Minister Liz Truss sent 10-year gilt yields soaring from about 3.5 percent to 4.5 percent in less than a week.

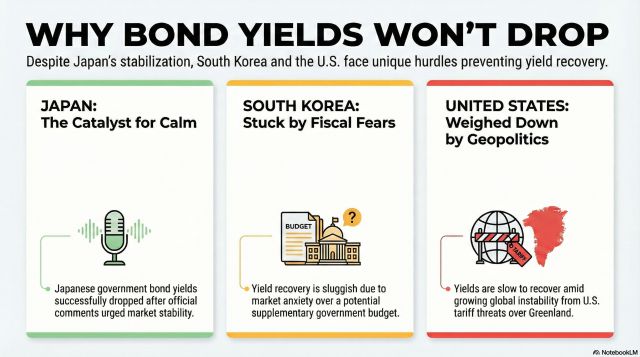

After Japanese Finance Minister Satsuki Katayama urged markets to “maintain calm,” the 10-year JGB yield slipped further, down 8.6 basis points to 2.29 percent.

The recovery in Korea has lagged.

The 10-year Korean yield stood at 3.619 percent on Wednesday morning, still up 3.4 basis points and failing to fully reverse the previous day’s sharp jump.

Part of the drag stemmed from Korea's own fiscal stimulus agenda. On Tuesday, President Lee Jae-myung mentioned the possibility of a supplementary budget, instructing Culture Minister Choi Hwi-young to review potential increases in arts and culture spending. Although Lee later clarified at a Wednesday press conference that there would be “no reckless supplementary budget,” the initial comment had already unsettled the bond market.

|

Generated with Notebook LM. |

U.S. Treasury yields also eased slightly, with the 10-year yield ending Wednesday at 4.275 percent, down 2 basis points, but still short of a full recovery. Persistent geopolitical risks — including Washington’s threat to impose a 10 percent tariff on countries opposing its push to acquire Greenland — continued to weigh on sentiment.

Caution urged over expansionary fiscal trends

While analysts say fears of a systemic shock in South Korea are overstated, they warn that a broader global tilt toward fiscal expansion among major currency issuers poses ongoing risks.

“Mentioning a supplementary budget in January is unusual, but South Korea is likely to exceed its tax revenue targets this year, making large-scale bond issuance unlikely,” said Kang Seung-won, a researcher at NH Securities. Kang added that a projected 30 percent increase in earnings among KOSPI and KOSDAQ-listed companies should help buffer the domestic bond market.

Still, expansionary fiscal policies elsewhere remain a concern.

“We are seeing a recurring pattern where fiscal concerns push up bond yields and market rates, which then weigh on currencies,” said Kwon Ah-min, another researcher at NH Securities.

Kwon pointed to Japan’s record 122.3 trillion yen budget for fiscal 2026 — with 29.6 trillion yen expected to be financed through debt — as a key risk factor.

“Rising bond issuance among major economies remains a volatile variable for global financial markets,” she said.

Kim Yeon-jae Reporter duswogmlwo77@ajupress.com

- Copyright ⓒ [아주경제 ajunews.com] 무단전재 배포금지 -