|

Graphics by AJP Song Ji-yoon |

|

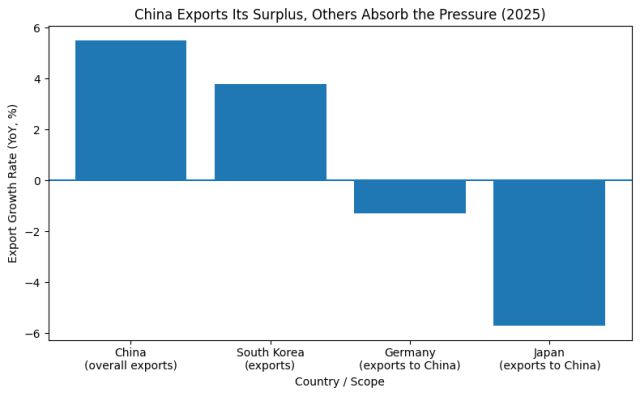

This ai generated graph show export growth comparison between China, South Korea, Germany and Japan (Chat GPT generated graphic) |

Export growth picked up to 6.6 percent in December, from 5.9 percent in November, while imports rose 5.7 percent, signaling that global demand for Chinese goods remained firm despite uneven domestic conditions.

Pivot away from the U.S. — and into third markets

|

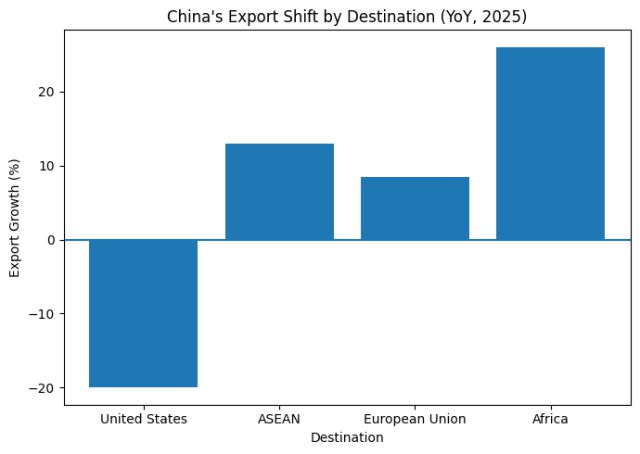

This AI generated graph show China’s Export Shift by Destination (Chat GPT generated graphic) |

China’s record surplus was sustained by a sharp geographical pivot. Exports to Southeast Asia rose 13 percent, shipments to the European Union climbed 8.4 percent, and exports to Africa surged 26 percent, as manufacturers redirected supply chains toward faster-growing regions.

Persistent producer-price deflation at home, combined with strong demand tied to artificial-intelligence investment, has kept Chinese goods highly competitive on price — intensifying head-to-head competition in third markets rather than expanding overall demand.

Korea: solid exports, but losing relative ground

For South Korea, where exports account for roughly 37 percent of GDP, China’s expanding footprint is reshaping competitive dynamics rather than collapsing trade outright.

Korea’s exports rose 3.8 percent in 2025 to a record $709.7 billion, surpassing the $700 billion mark for the first time and delivering a $78 billion trade surplus, according to the Ministry of Trade, Industry and Energy. Semiconductor shipments surged 22.2 percent, driven by AI-related demand, while automobiles and shipbuilding also posted record values.

Yet in relative terms, Korea is losing ground. While China’s exports grew more than twice as fast, Korea’s export growth remained modest, pushing the country down to eighth in global export rankings, from sixth a year earlier. Korean firms face narrowing margins in semiconductors, batteries, steel and industrial machinery, as price-based competition with Chinese suppliers intensifies across ASEAN, India and the Middle East.

“China’s expanding export footprint is reshaping competitive dynamics in third markets, where Korean and Chinese firms increasingly overlap,” said Heo Seul-bi, an analyst at the Korea International Trade Association. “As Chinese shipments shift toward ASEAN, India and Africa amid higher U.S. tariffs, head-to-head competition has become more pronounced, particularly in price-sensitive sectors such as steel and basic industrial materials.”

Germany: widening imbalance at Europe’s industrial core

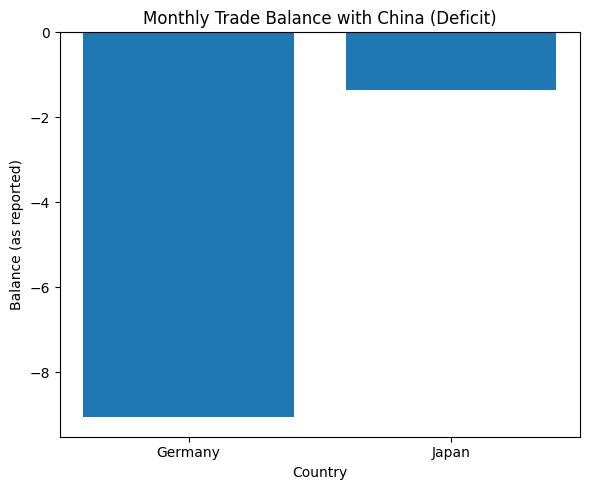

The pressure is even more visible in Germany, Europe’s manufacturing anchor. In September 2025, Germany exported €6.77 billion ($7.4 billion) to China while importing €15.8 billion, resulting in a monthly trade deficit of €9.06 billion.

Compared with a year earlier, German exports to China edged down 1.3 percent, while imports surged 8.68 percent, highlighting the accelerating asymmetry in bilateral trade flows. Rising imports of Chinese machinery, automobiles and data-processing equipment have weighed on factory orders and industrial output, which remain below pre-pandemic levels.

|

This AI generated graphic show Germany and Japan's monthly trade balance with China (Chat GPT generated graphic) |

Japan: shifting balance inside the supply chain

Japan faces a different, but equally revealing, adjustment. In October 2025, China exported $13.0 billion to Japan while importing $14.4 billion, leaving China with a $1.35 billion bilateral trade deficit.

China’s exports to Japan fell 5.7 percent year on year, driven by steep declines in shipments of telephones, railway cargo containers and ships. At the same time, imports from Japan jumped 5.9 percent, led by a more than 70 percent surge in integrated circuits, alongside automobiles and industrial materials such as scrap copper.

The data point to Japan’s continued strength in high-end components, but also underline its growing exposure to competition from China in finished manufacturing goods.

China’s surplus reflects domestic imbalance — exported abroad

Economists warn that China’s surplus is not merely a sign of export strength, but also of domestic imbalance. Heavy investment in machinery and equipment — increasingly led by state-owned enterprises — has expanded production capacity, while household consumption has lagged amid weak confidence, falling property values and precautionary saving.

With deflationary pressures at home, surplus output has flowed abroad. U.S. tariffs have diverted, rather than stopped, Chinese exports — shifting adjustment costs onto other economies.

“Unlike the U.S., which continues to absorb imports amid strong growth, many advanced economies are struggling,” one trade economist said. “Chinese exports are landing in markets where manufacturers are already under strain.”

Fragmentation risks grow

Governments are beginning to respond. French President Emmanuel Macron has raised trade imbalances directly with Beijing, while European Commission President Ursula von der Leyen has warned that Europe risks becoming a dumping ground for Chinese goods. Mexico has raised tariffs on Chinese imports, and other countries are weighing similar measures.

China continues to frame itself as a defender of free trade. But analysts argue that relying on the rest of the world to absorb domestic imbalances risks accelerating trade fragmentation, especially as geopolitical blocs harden.

For South Korea, Germany and Japan, the challenge is not a collapse in exports, but relative erosion — competing against a China that is exporting its surplus, its deflation and its industrial overcapacity into the same global markets.

Yoo Joonha Reporter joonhayoo94@ajupress.com

- Copyright ⓒ [아주경제 ajunews.com] 무단전재 배포금지 -